Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Inflation Affects the Housing Market

Have you ever wondered how inflation impacts the housing market? Believe it or not, they’re connected. Whenever there are changes to one, both are affected. Here’s a high-level overview of the connection between the two.

The Relationship Between Housing Inflation and Overall Inflation

Shelter inflation is the measure of price growth specific to housing. It comes from a survey of renters and homeowners that’s done by the Bureau of Labor Statistics (BLS). The survey asks renters how much they’re paying in rent, and homeowners how much they’d rent their homes for, if they weren’t living in them.

Much like overall inflation measures the cost of everyday items, shelter inflation measures the cost of housing. And for four consecutive months, based on that survey, shelter inflation has been coming down (see graph below):

Why does this matter? Well, shelter inflation makes up about one-third of overall inflation, as measured by the Consumer Price Index (CPI). So, when shelter inflation moves, it leads to noticeable moves in overall inflation. That means the recent dip in shelter inflation might be a sign that overall inflation could fall in the months ahead.

Why does this matter? Well, shelter inflation makes up about one-third of overall inflation, as measured by the Consumer Price Index (CPI). So, when shelter inflation moves, it leads to noticeable moves in overall inflation. That means the recent dip in shelter inflation might be a sign that overall inflation could fall in the months ahead.

That moderation would be a welcome sight for the Federal Reserve (the Fed). They’ve been working to get inflation under control since early 2022. While they’ve made some headway (it peaked at 8.9% in the middle of last year), they’re still trying to get to their 2% goal (the latest report is 3.3%).

Inflation and the Federal Funds Rate

What’s the Fed been doing to lower inflation? They’ve been increasing the Federal Funds Rate. That interest rate influences how much it costs banks to borrow money from each other. When inflation climbed, the Fed responded by raising the Federal Funds Rate to keep the economy from overheating.

The graph below shows the relationship between the two. Each time inflation (shown in the blue line) starts to climb, the Fed raises the Federal Funds Rate (shown in the orange line) to try to get it back to their target of 2% (see below):

The circled portion of the graph shows the most recent spike in inflation, the Fed’s actions to raise the Federal Funds Rate to fight that, and the moderation of inflation that happened in response to that hike. As inflation gets closer to the Fed’s current 2% goal, they may not need to raise the Federal Funds Rate much further.

The circled portion of the graph shows the most recent spike in inflation, the Fed’s actions to raise the Federal Funds Rate to fight that, and the moderation of inflation that happened in response to that hike. As inflation gets closer to the Fed’s current 2% goal, they may not need to raise the Federal Funds Rate much further.

A Brighter Future for Mortgage Rates?

So, what does all of this mean for you? While the actions coming out of the Fed don’t determine mortgage rates, they do have an impact. As Mortgage Professional America (MPA) explains:

“. . . mortgage rates and inflation are connected, however indirectly. When inflation rises, mortgage rates rise to keep up with the value of the US dollar. When inflation drops, mortgage rates follow suit.”

While no one can predict the future of mortgage rates, it’s encouraging to see the signs of moderating inflation in the economy.

Buyer Traffic Is Still Stronger than the Norm

Are you putting off selling your house because you’re worried no one’s buying because of where mortgage rates are? If so, know this: the latest data shows plenty of buyers are still out there, and they’re purchasing homes today. Here’s the data to prove it.

The ShowingTime Showing Index is a measure of buyers touring homes. The graph below uses the latest numbers available and compares them to the same month in the last normal years to show just how active today’s buyers still are:

As you can see, when June 2023 numbers are stacked alongside what’s typical for the housing market at this time of year, it’s clear buyers are still active. And, they’re actually a lot more active than the norm.

As you can see, when June 2023 numbers are stacked alongside what’s typical for the housing market at this time of year, it’s clear buyers are still active. And, they’re actually a lot more active than the norm.

If you’re wondering how this could possibly be true, it’s because buyers are getting used to higher mortgage rates and accepting them as the new reality. As Danielle Hale, Chief Economist, Realtor.com, explains:

“Interest rate hikes continue to further cut into buyers’ purchasing power, although they appear to have adapted to the higher mortgage rate environment . . .”

It’s simple. Buyers will always need to buy, and those who can afford to move at today’s rates are going to do so.

The Key Takeaway for You

While it’s true things have slowed down from the frenzy of the last couple of years, it doesn’t mean today’s market is at a standstill. The reality is: buyer traffic is still strong today. Even with today’s mortgage rates, plenty of buyers are still making their moves. So why delay your own move when there’s clearly a market for your house?

Bottom Line

Don’t put off your plans because you’re worried no one will buy your home. The opposite is true, and more buyers are more active than the norm. Let’s connect to get your house ready to sell, so it makes the best first impression possible on those eager buyers.

Why You May Still Want To Sell Your House After All

Even though you may feel reluctant to sell your house because you don’t want to take on a mortgage rate that’s higher than the one you have now, there’s more to consider. While the financial side of things does matter, your personal needs may actually matter just as much. As an article from Bankrate says:

“Deciding whether it’s the right time to sell your home is a very personal decision. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market.”

So, ask yourself this: why did I want to move in the first place?

Chances are your primary motivation wasn’t just financial in nature. Why you’re really thinking about selling likely has more to do with something changing in your life or a shift in what you need out of your house.

Reasons Homeowners Still Need To Sell Today

Let’s explore some of the most common reasons sellers are moving today. A recent article from Builder Online helps shed light on this. In this research, they identified the following categories:

- Marriage – If you just got married, you may find you either need more space than you currently have, or the two of you want to find a new place you picked out together.

- Divorce – If you’re getting separated or are divorcing your partner, chances are it’ll be difficult to live under the same roof. Selling the place you have, so you can own get your own spot, may be necessary.

- Births – If your household is growing, you may need more square footage, including more bedrooms. If you’re running out of room for everyone, you may not be able to wait to move.

- Deaths – If you’ve recently lost a loved one, it can be hard to spend time in that home. You may need to move for financial reasons or because you no longer need all the space.

- Retirement – If you’re in the process of retiring, or you just did, you may be looking to downsize to cut costs, relocate to be closer to loved ones, or move to a dream location. In this new phase of life, your current home may not be able to deliver what you need.

You may find you share one of these top motivators. If any of these resonate with you, it may be time to move so you can find a house better suited to your changing needs. A survey from Realtor.com finds other sellers are in the same boat. It says, 1 in 4 sellers are choosing to move for personal reasons, even with current mortgage rates:

“. . . more than half of seller-buyers (56%) who are planning to sell in the next 12 months said they are waiting for rates to come down, while 25% need to sell soon for personal reasons.”

If you need to sell now because something in your own life has changed, don’t let rates hold you back from what you want. You have options to help make that move possible. You can use the equity you already have in your current home toward your next purchase. And with how much equity homeowners have right now, you may be able to finance less than you’d expect or pay all cash to avoid borrowing at all.

Bottom Line

When you’re ready to prioritize your changing needs, let’s connect. You need an expert on your side to help you list your house and find a home that delivers everything you’re looking for.

Gen Z: The Next Generation Is Making Moves in the Housing Market

Generation Z (Gen Z) is eager to put down their own roots and achieve financial independence. As a result, they’re turning to homeownership. According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), 30% of Gen Z buyers transitioned straight from living under their parents’ roofs to owning their own homes.

If you’re a member of this generation, and you’re interested in pursuing your own dream of homeownership, here’s some information you may find helpful on why and where your peers are buying.

The Reasons Gen Z Want To Become Homeowners

A recent survey by Rocket Mortgage identifies some of the top motivators driving Gen Z buyers to purchase a home:

“Of those surveyed, 34% said that starting or growing their family was their main motivation to buy a home. . . . Along with growing a family comes establishing a home base.”

Another key reason the survey says Gen Z wants to buy is because homeownership can give them more stability (20.8%). That’s because buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost.

When you have a fixed-rate mortgage on your home, you can lock in your monthly payment for the duration of your loan, often 15 to 30 years. If you keep renting, you don’t have that same benefit, and you won’t be protected from rising housing costs.

So, if you’re ready to start a new chapter in your life or if you’re craving more stability, know that your peers feel the same way, and those motivators are why they’re turning to homeownership.

Gen Z’s Next Stop: Where Are They Making Their Moves?

If those reasons have you feeling ready to buy, here’s some information on where your peers are finding their homes that could help you with your search. According to a recent Lending Tree survey, Gen Z buyers are focusing on more affordable areas to help boost their buying power and offset the challenges that come with today’s mortgage rates.

Many Gen Z buyers still want the convenience and excitement of city life, but also value the affordability, open air, and space more suburban areas offer. Jacob Channel, Senior Economist at LendingTree, explains:

“. . . they want to live in a city, but they also want to be close to nature.”

Locating a home that offers both of those things requires expertise. Working with a trusted real estate professional can help you find a home in your budget and desired area. Your agent will know the most affordable neighborhoods to search in. They can also highlight the amenities and features that location offers and how those are aligned with your goals. They’ll also be able to walk you through how things like remote work can help you cast a broader net for your search.

Bottom Line

If you’re a member of Gen Z and are just getting started on your homebuying journey, or if you want to learn more about the process, let’s connect. That way, you have a guide to help you find a home that fits both your lifestyle and your budget.

Today’s Housing Market Has Only Half the Usual Inventory [INFOGRAPHIC]

More Jobs and Better Pay Leads to More Buyer Demand

There’s been talk about a recession for quite a while now. But the economy has been remarkably resilient. Why? One reason is employment and wages have stayed strong. Let’s look at the latest information on each one and why both are good news if you’re thinking about selling your house.

More Jobs Are Being Created

Instead of facing the job losses typical of any recession, the economy has been growing and adding jobs. According to the Bureau of Labor Statistics (BLS), 187,000 jobs were created in July, which is up from the 185,000 created in June. That means more people are finding work. In fact, so many jobs are being added that the unemployment rate is far lower than the long-term average of 5.7% (see graph below):

A low unemployment rate means that most people who want to work are finding jobs. When people have jobs, they have steady incomes – and that can help set them up to consider homeownership.

People Are Making More Money

Data also shows hourly earnings have been going up pretty steadily over the past few years (see graph below):

When wages rise, people have more money that they could save or use toward buying a home. This increase in income helps offset some of the affordability challenges in the housing market today. Affordability depends on three main factors: wages, home prices, and mortgage rates. With higher home prices and mortgage rates right now, Builder Online summarizes how growing wages can help:

“The housing market has been a beneficiary of the strong economy and labor market. Many of those employed have saved money over the past few years and used those funds toward a down payment on a home.”

If you’re thinking about selling your house, a strong job market, growing wages, and the resulting buyer demand is fantastic news. It means there’s a larger pool of potential buyers out there who are in a position to pursue their dreams of homeownership.

Bottom Line

With more jobs and rising wages creating eager buyers, there’s a lot going in your favor. Let’s connect so you have someone who can guide you through the process of selling your house, from setting the right price to getting your home ready to show.

Why You Need a True Expert in Today’s Housing Market

The housing market continues to shift and change, and in a fast-moving landscape like we’re in right now, it’s more important than ever to have a trusted real estate agent on your side. Whether you’re buying your first home or selling once again, it’s mission critical to work with an expert who can guide you through each unique step of the process.

The reality is, not all agents operate the same way. To truly make a powerful and confident decision as you buy or sell a home, you need a real estate expert who uses their knowledge of what’s really happening with home prices, housing supply, industry projections, and more to give you the best possible advice. Someone who can provide clarity and trust like that is essential to your success. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty for consumers. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You can lean on an expert to help you separate fact from fiction and get the answers you need.

The right agent can assist you in figuring out what’s going on at the national level and in your local area. They can debunk headlines using data you can trust. Experts have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you want sound advice and trusted information about our local housing market, give me a shout!

Why You Don’t Need To Fear the Return of Adjustable-Rate Mortgages

If you remember the housing crash back in 2008, you may recall just how popular adjustable-rate mortgages (ARMs) were back then. After years of being virtually nonexistent, more people are once again using ARMs when buying a home. Let’s break down why that’s happening and why this isn’t cause for concern.

Why ARMs Have Gained Popularity More Recently

This graph uses data from the Mortgage Bankers Association (MBA) to show how the percentage of adjustable-rate mortgages has increased over the past few years:

As the graph conveys, after hovering around 3% of all mortgages in 2021, many more homeowners turned to adjustable-rate mortgages again last year. There’s a simple explanation for that increase. Last year, mortgage rates climbed dramatically. With higher borrowing costs, some homeowners decided to take out this type of loan because traditional borrowing costs were high, and an ARM gave them a lower rate.

Why Today’s ARMs Aren’t Like Those in 2008

To put things into perspective, let’s remember these aren’t like the ARMs that became popular leading up to 2008. Part of what caused the housing crash was loose lending standards. Back then, when a buyer got an ARM, banks and lenders didn’t require proof of their employment, assets, income, etc. Basically, people were getting loans that they shouldn’t have, which set many homeowners up for trouble because they couldn’t pay back the loans that they never had to qualify for in the first place.

This time around, lending standards are different. Banks and lenders learned from the crash, and now they verify income, assets, employment, and more. This means today’s buyers actually have to qualify for their loans and show they’ll be able to repay them.

Archana Pradhan, Economist at CoreLogic, explains the difference between then and now:

“Around 60% of Adjustable-Rate Mortgages (ARM) that were originated in 2007 were low- or no-documentation loans . . . Similarly, in 2005, 29% of ARM borrowers had credit scores below 640 . . . Currently, almost all conventional loans, including both ARMs and Fixed-Rate Mortgages, require full documentation, are amortized, and are made to borrowers with credit scores above 640.”

In simple terms, Laurie Goodman at Urban Institute helps drive this point home by saying:

“Today’s Adjustable-Rate Mortgages are no riskier than other mortgage products and their lower monthly payments could increase access to homeownership for more potential buyers.”

Bottom Line

If you’re worried today’s adjustable-rate mortgages are like the ones from the housing crash, rest assured, things are different this time. If you’re a first-time homebuyer and you’d like to learn more about lending options that could help you overcome today’s affordability challenges, reach out to a trusted lender.

Why Median Home Sales Price Is Confusing Right Now

The National Association of Realtors (NAR) is set to release its most recent Existing Home Sales (EHS) report tomorrow. This monthly release provides information on the volume of sales and price trends for homes that have previously been owned. In the upcoming release, it’ll likely say home prices are down. This may seem a bit confusing, especially if you’ve been following along and reading the blogs saying home prices have hit the bottom and have since rebounded.

So, why would this say home prices are falling when so many other price reports say they’re going back up? It all depends on the methodology of each one. NAR reports on the median home sales price, while some other sources use repeat sales prices. Here’s how those approaches differ.

The Center for Real Estate Studies at Wichita State University explains median sales prices like this:

“The median sale price measures the ‘middle’ price of homes that sold, meaning that half of the homes sold for a higher price and half sold for less . . . For example, if more lower-priced homes have sold recently, the median sale price would decline (because the “middle” home is now a lower-priced home), even if the value of each individual home is rising.”

Investopedia helps define what a repeat sales approach means:

“Repeat-sales methods calculate changes in home prices based on sales of the same property, thereby avoiding the problem of trying to account for price differences in homes with varying characteristics.”

The Challenge with the Median Home Sales Price Today

As the quotes above say, the approaches can tell different stories. That’s why median home sales price data (like EHS) may say prices are down, even though the vast majority of the repeat sales reports show prices are appreciating again.

Bill McBride, Author of the Calculated Risk blog, sums the difference up like this:

“Median prices are distorted by the mix and repeat sales indexes like Case-Shiller and FHFA are probably better for measuring prices.”

To drive this point home, here’s a simple explanation of median value (see visual below). Let’s say you have three coins in your pocket, and you decide to line them up according to their value from low to high. If you have one nickel and two dimes, the median value (the middle one) is 10 cents. If you have two nickels and one dime, the median value is now five cents.

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change.

That’s why using the median home sales price as a gauge of what’s happening with home values may be confusing right now. Most buyers look at home prices as a starting point to determine if they match their budgets. But most people buy homes based on the monthly mortgage payment they can afford, not just the price of the house. When mortgage rates are higher, you may have to buy a less expensive home to keep your monthly housing expenses affordable.

That’s why a greater number of ‘less-expensive’ houses are selling right now – and that’s causing the median home sales price to decline. But that doesn’t mean any single house lost value.

When you see the stories in the media that prices are falling later this week, remember the coins. Just because the median home sales price changes, it doesn’t mean home prices are falling. What it means is the mix of homes being sold is being impacted by affordability and current mortgage rates.

Bottom Line

For a more in-depth understanding of home price trends and reports, don’t hesitate to reach out.

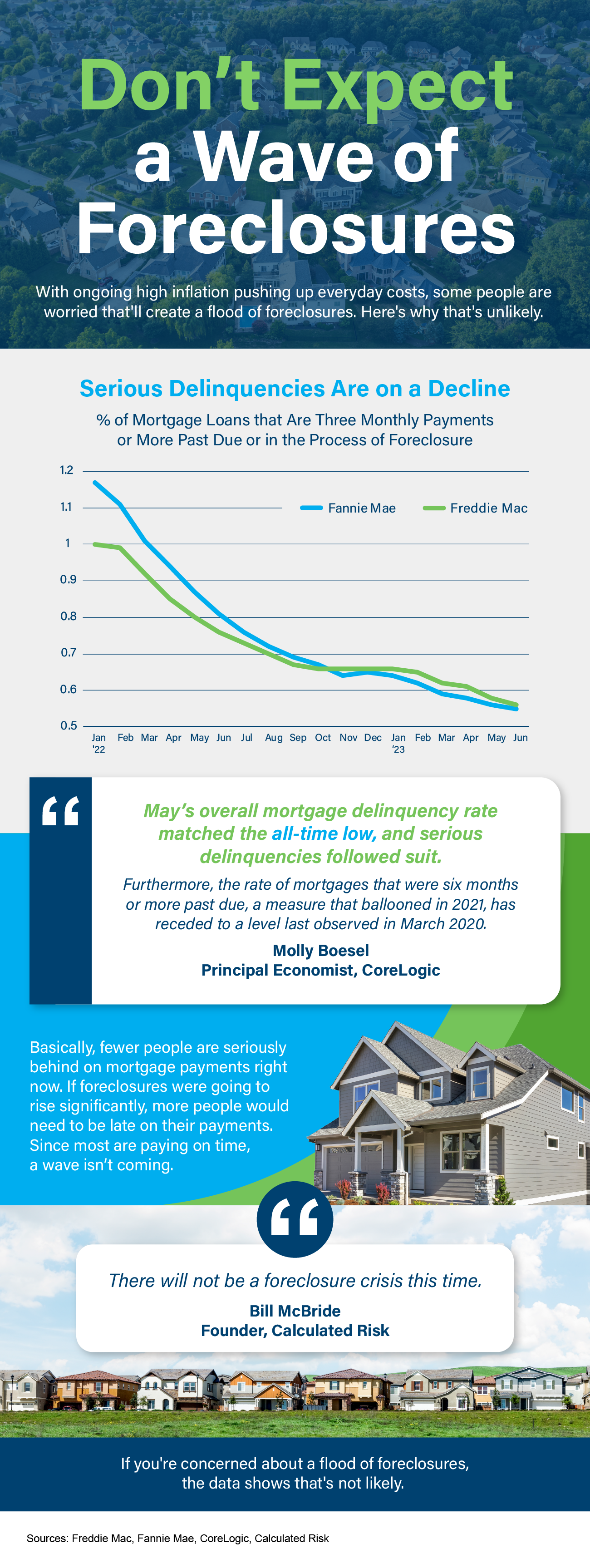

Don’t Expect a Wave of Foreclosures [INFOGRAPHIC]

Some Highlights

- With ongoing high inflation pushing up everyday costs, some people are worried that’ll create a flood of foreclosures. Here’s why that’s unlikely.

- Fewer people are seriously behind on mortgage payments right now. If foreclosures were going to rise a lot, more people would need to be late on their payments.

- Since most are paying on time, a wave isn’t coming. If you’re concerned about a flood of foreclosures, the data shows that’s not likely.