Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

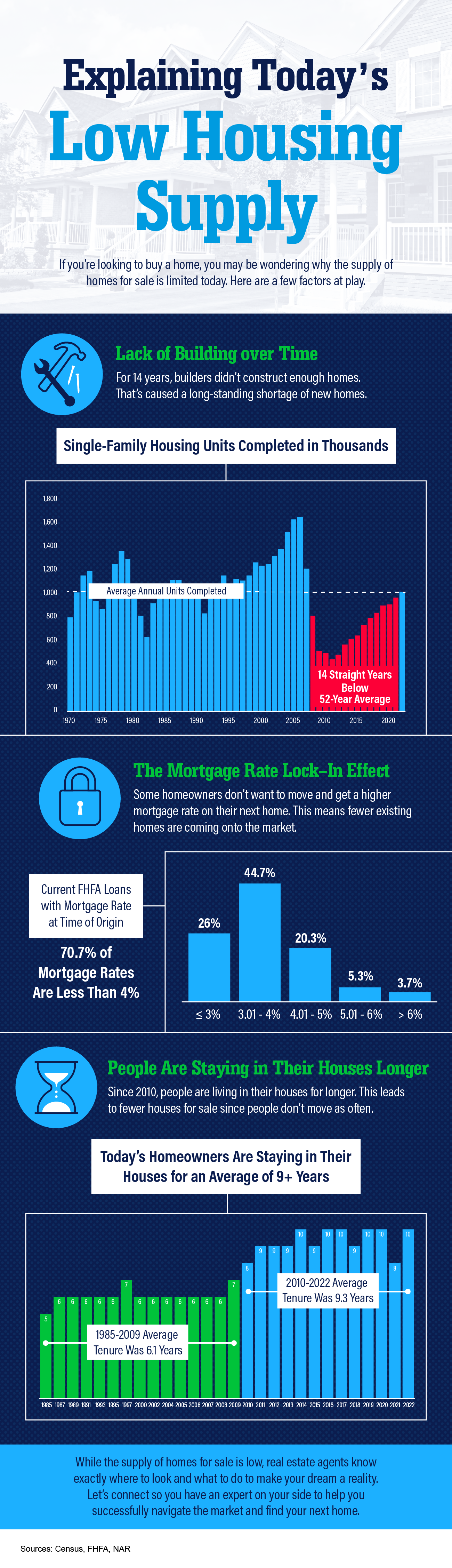

Explaining Today’s Low Housing Supply [INFOGRAPHIC]

Some Highlights

- Wondering why the supply of homes for sale is limited today? There are a few factors at play.

- Lack of building over time, the mortgage rate lock-in effect, and people staying in their houses longer are three of the main reasons why supply is low.

- But real estate agents know exactly where to look and what to do to make your dream a reality. Let’s chat so you have an expert on your side to help you successfully navigate the market and find your next home.

Why Your House Didn’t Sell

If your listing expired and your house didn’t sell, you’re likely feeling a little frustrated. Not to mention, you’re also probably wondering what went wrong. Here are three questions to think about as you figure out what to do next.

Did You Limit Access to Your House?

One of the biggest mistakes you can make when selling your house is restricting the days and times when potential buyers can tour it. Being flexible with your schedule is important when you’re selling your house, even though it might feel a bit stressful to drop everything and leave when buyers want to see it. After all, minimal access means minimal exposure to buyers. ShowingTime advises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

Sometimes, the most determined buyers might come from far away. Since they’re traveling to see your house, they may not be able to change their plans easily if you only offer limited times for showings. So, try to make your house available as much as you can to accommodate them. It’s simple. If no one’s able to look at it, how’s it going to sell?

Did You Make Your House Stand Out?

When selling your house, the old saying matters: you never get a second chance to make a first impression. Putting in the work to make the exterior of your home look nice is just as important as how you stage it inside. Freshen up your landscaping to improve your home’s curb appeal so you can make an impact upfront. As an article from U.S. News says:

“After all, if people drive by, but aren’t interested enough to walk through the front door, you’ll never sell your house.”

But don’t let that impact stop at the front door. By removing personal items and reducing clutter inside, you give buyers more freedom to picture themselves in the home. Additionally, a new coat of paint or cleaning the floors can go a long way to freshening up a room.

Did You Price Your House Compellingly?

Setting the right price is extremely important when you’re selling your house. Even though it might feel tempting to push the price higher to maximize your profit, overpricing can scare away buyers and make it hard to sell quickly. Business Insider notes:

“. . . the biggest mistake sellers make is overpricing their home.”

If your house is priced higher than others like it, it could make buyers lose interest. Pay attention to the feedback people give your agent during open houses and showings. If lots of people are saying the same thing, it might be a good idea to think about lowering the price.

For all these insights and more, rely on a trusted real estate agent. A great agent will offer expert advice on relisting your house with effective strategies to get it sold.

Bottom Line

It’s natural to feel disappointed when your listing has expired and your house didn’t sell. Let’s chat to figure out what happened and what to reconsider or change if you want to get your house back on the market.

Why Today’s Housing Inventory Shows a Crash Isn’t on the Horizon

You might remember the housing crash in 2008, even if you didn’t own a home at the time. If you’re worried there’s going to be a repeat of what happened back then, there’s good news – the housing market now is different from 2008.

One important reason is there aren’t enough homes for sale. That means there’s an undersupply, not an oversupply like the last time. For the market to crash, there would have to be too many houses for sale, but the data doesn’t show that happening.

Housing supply comes from three main sources:

- Homeowners deciding to sell their houses

- Newly built homes

- Distressed properties (foreclosures or short sales)

Here’s a closer look at today’s housing inventory to understand why this isn’t like 2008.

Homeowners Deciding To Sell Their Houses

Although housing supply did grow compared to last year, it’s still low. The current months’ supply is below the norm. The graph below shows this more clearly. If you look at the latest data (shown in green), compared to 2008 (shown in red), there’s only about a third of that available inventory today.

So, what does this mean? There just aren’t enough homes available to make home values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that’s not happening.

Newly Built Homes

People are also talking a lot about what’s going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. The graph below shows the number of new houses built over the last 52 years:

The 14 years of underbuilding (shown in red) is a big part of the reason why inventory is so low today. Basically, builders haven’t been building enough homes for years now and that’s created a significant deficit in supply.

While the final blue bar on the graph shows that’s ramping up and is on pace to hit the long-term average again, it won’t suddenly create an oversupply. That’s because there’s too much of a gap to make up. Plus, builders are being intentional about not overbuilding homes like they did during the bubble.

Distressed Properties (Foreclosures and Short Sales)

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back during the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from the Federal Reserve to show how things have changed since the housing crash:

This graph illustrates, as lending standards got tighter and buyers were more qualified, the number of foreclosures started to go down. In 2020 and 2021, the combination of a moratorium on foreclosures and the forbearance program helped prevent a repeat of the wave of foreclosures we saw back around 2008.

The forbearance program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. Data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

What This Means for You

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. According to Bankrate, that isn’t going to change anytime soon, especially considering buyer demand is still strong:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

Bottom Line

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing inventory tells us there’s no crash on the horizon.

The Return of Normal Seasonality for Home Price Appreciation

If you’re thinking of making a move, one of the biggest questions you have right now is probably: what’s happening with home prices? Despite what you may be hearing in the news, nationally, home prices aren’t falling. It’s just that price growth is beginning to normalize. Here’s the context you need to really understand that trend.

In the housing market, there are predictable ebbs and flows that happen each year. It’s called seasonality. Spring is the peak homebuying season when the market is most active. That activity is typically still strong in the summer but begins to wane as the cooler months approach. Home prices follow along with seasonality because prices appreciate most when something is in high demand.

That’s why there’s a reliable long-term home price trend. The graph below uses data from Case-Shiller to show typical monthly home price movement from 1973 through 2022 (not adjusted, so you can see the seasonality):

As the data shows, at the beginning of the year, home prices grow, but not as much as they do in the spring and summer markets. That’s because the market is less active in January and February since fewer people move in the cooler months. As the market transitions into the peak homebuying season in the spring, activity ramps up, and home prices go up a lot more in response. Then, as fall and winter approach, activity eases again. Price growth slows, but still typically appreciates.

After several unusual ‘unicorn’ years, today’s higher mortgage rates helped usher in the first signs of the return of seasonality. As Selma Hepp, Chief Economist at CoreLogic, explains:

“High mortgage rates have slowed additional price surges, with monthly increases returning to regular seasonal averages. In other words, home prices are still growing but are in line with historic seasonal expectations.”

Why This Is So Important to Understand

In the coming months, you’re going to see the media talk more about home prices. In their coverage, you’ll likely see industry terms like these:

- Appreciation: when prices increase.

- Deceleration of appreciation: when prices continue to appreciate, but at a slower or more moderate pace.

- Depreciation: when prices decrease.

Don’t let the terminology confuse you or let any misleading headlines cause any unnecessary fear. The rapid pace of home price growth the market saw in recent years was unsustainable. It had to slow down at some point and that’s what we’re starting to see – deceleration of appreciation, not depreciation.

Remember, it’s normal to see home price growth slow down as the year goes on. And that definitely doesn’t mean home prices are falling. They’re just rising at a more moderate pace.

Bottom Line

While the headlines are generating fear and confusion about what’s happening with home prices, the truth is simple. Home price appreciation is returning to normal seasonality. If you have questions about what’s happening with prices in our local area, don’t hesitate to reach out.

Beginning with Pre-Approval

If you’re looking to buy a home this fall, there are a few things you need to know. Affordability is tight with today’s mortgage rates and rising home prices. At the same time, there’s a limited number of homes on the market right now and that’s creating some competition among buyers. But, if you’re strategic, there are ways to navigate these waters. The first thing you’ll want to do is get pre-approved for a mortgage. That way you’ll know your numbers and can set yourself up for success from the start of your home search.

What Pre-Approval Does for You

To understand why it’s such an important step, you need to know what pre-approval is. As part of the homebuying process, a lender looks at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you know how much money you can borrow. Freddie Mac explains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Basically, pre-approval gives you critical information about the home buying process that’ll help you understand how much you may be able to borrow. Why does this help you, especially today? With higher mortgage rates and home prices impacting affordability for many buyers right now, a solid understanding of your numbers is even more important so you can truly wrap your head around your options.

Pre-Approval Helps Show Sellers You’re a Serious Buyer

Let’s face it, there are more buyers looking to buy than there are homes available for sale and that imbalance is creating some competition among home buyers. That means you could see yourself in a multiple-offer scenario when you make an offer on a home. Getting pre-approved for a mortgage can help you stand out from other hopeful buyers.

As an article from the Wall Street Journal (WSJ) says:

“If you plan to use a mortgage for your home purchase, preapproval should be among the first steps in your search process. Not only can getting preapproved help you zero in on the right price range, but it can give you a leg up on other buyers, too.”

Pre-approval shows the seller you’re a serious buyer who has already undergone a credit and financial check, making it more likely that the sale will move forward without unexpected delays or financial issues.

Bottom Line

Getting pre-approved is an important first step when you’re buying a home. The more prepared you are, the better chance you have of getting the home you want. Connect with a trusted lender so you have the tools you need to purchase a home in today’s market.

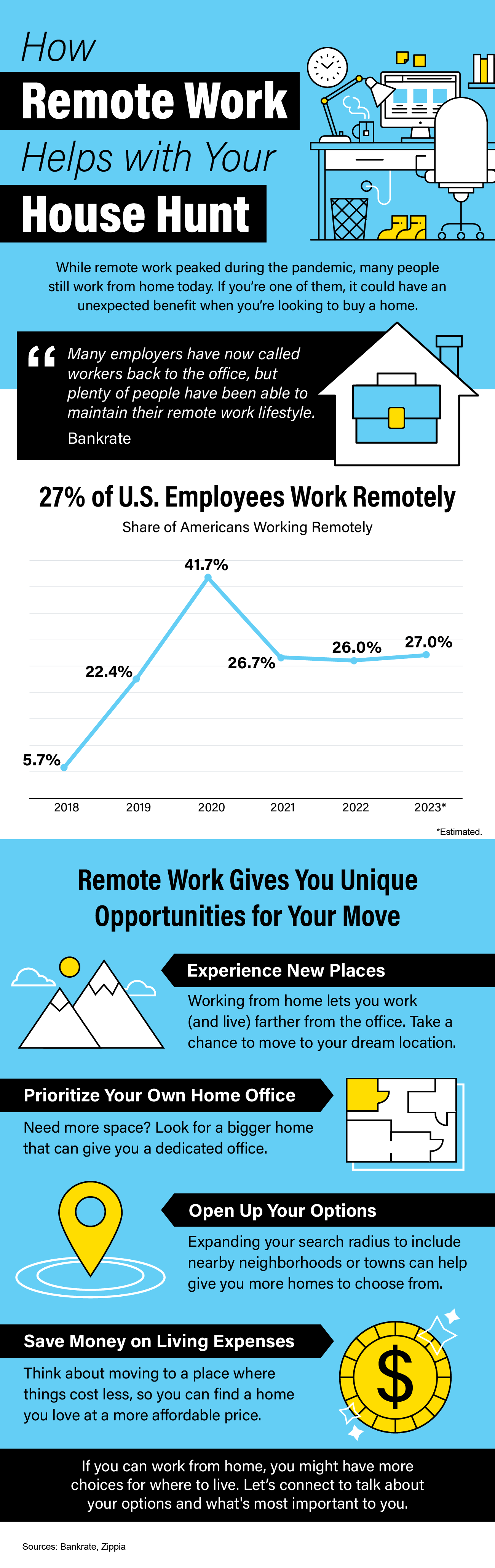

How Remote Work Helps with Your House Hunt [INFOGRAPHIC]

Some Highlights

- While remote work peaked during the pandemic, many people still work from home today.

- If you’re one of them, it could have an unexpected benefit when you’re looking to buy a home.

- If you can work from home, you might have more choices for where to live.

The Many Non-Financial Benefits of Homeownership

Buying and owning your own home can have a big impact on your life. While there are financial reasons to become a homeowner, it’s essential to think about the non-financial benefits that make a home more than just a place to live.

Here are some of the top non-financial reasons to buy a home.

According to Fannie Mae, 94% of survey respondents say “Having Control Over What You Do with Your Living Space” is a top reason to own.

Your home is truly your own space. If you own a home, unless there are specific homeowner association requirements, you can decorate and change it the way you like. That means you can make small changes or even do big renovations to make your home perfect for you. Your home is uniquely yours and by buying, you give yourself the freedom to tailor it to your individual style. Investopedia explains:

“One often-cited benefit of homeownership is the knowledge that you own your little corner of the world. You can customize your house, remodel, paint, and decorate without the need to get permission from a landlord.”

When you rent, you might not be able to make your place really feel like it’s yours. And if you do make any modifications, you might have to change them back before you leave. But if you own your home, you can make it just the way you want it. That level of customization can give you a sense of pride in where you live and make you feel more connected to it.

Fannie Mae also finds 90% say “Having a Good Place for Your Family To Raise Your Children” tops their list of why it’s better to buy a home.

Another important factor to think about is what stage of life you’re in. U.S. News breaks it down:

“For those with young children, buying a home and putting down roots is a major driver. . . . You don’t want the upheaval of a massive rent increase or a non-renewed lease to impact your sense of stability.”

No matter which of life’s milestones you’re in, stability and predictability are important. That’s because the one constant in life is that things will change. And, as life changes around you, having a familiar home and not worrying about moving regularly helps you and those who matter most feel more secure and more comfortable.

Lastly, Fannie Mae says 82% list “Feeling Engaged in Your Community” as another key motivator to own.

Owning your home also helps you feel even more connected to your neighborhood. People who own homes usually live in them for an average of nine years, according to the National Association of Realtors (NAR). As that time passes, it’s natural to make friends and build strong ties in the community. As Gary Acosta, CEO and Co-Founder at the National Association of Hispanic Real Estate Professionals (NAHREP), points out:

“Homeowners also tend to be more active in their local communities . . .”

When you care deeply about the people you live near, you’ll do what you can to contribute to your local area.

Bottom Line

Owning your home can make your life better by giving you a sense of accomplishment, pride, stability, and connectedness.

Remote Work Is Changing How Some Buyers Search for Their Dream Homes

The way Americans work has changed in recent years, and remote work is at the forefront of this shift. Experts say it’ll continue to be popular for years to come and project that 36.2 million Americans will be working remotely by 2025. To give you some perspective, that’s a 417% increase compared to the pre-pandemic years when there were just 7 million remote workers.

If you’re in the market to buy a home and you work remotely either full or part-time, this trend is a game-changer. It can help you overcome some of today’s affordability and housing inventory challenges.

How Remote Work Helps with Affordability

Remote or hybrid work allows you to change how you approach your home search. Since you’re no longer commuting every day, you may not feel it’s as essential to live near your office. If you’re willing to move a bit further out in the suburbs instead of the city, you could open up your pool of affordable options. In a recent study, Fannie Mae explains:

“Home affordability may also be a reason why we saw an increase in remote workers’ willingness to relocate or live farther away from their workplace . . .”

If you’re thinking about moving, having this kind of location flexibility can boost your chances of finding a home that fits your budget. Work with your agent to cast a wider net that includes additional areas with a lower cost of living.

More Work Flexibility Means More Home Options

As you broaden your search to include more affordable options, you may also find you have the chance to get more features for your money too. Given the low supply of homes for sale, finding a home that fits all your wants and needs can be challenging.

By opening up your search, you’ll give yourself a bigger pool of options to choose from, and that makes it easier to find a home that truly fits your lifestyle. This could include homes with more square footage, diverse home styles, and a wider range of neighborhood amenities that were previously out of reach.

Historically, living close to work was a sought-after perk, often coming with a hefty price tag. But now, the dynamics have changed. If you work from home, you have the freedom to choose where you want to live without the burden of long daily commutes. This shift allows you to focus more on finding a home that is affordable and delivers on your dream home features.

Bottom Line

Remote work goes beyond job flexibility. It’s a chance to broaden your horizons in your home search. Without being bound to a fixed location, you have the freedom to explore all of your options.

Your Home Equity Can Offset Affordability Challenges

Are you thinking about selling your house? If so, today’s mortgage rates may be making you wonder if that’s the right decision. Some homeowners are reluctant to sell and take on a higher mortgage rate on their next home. If you’re worried about this too, know that even though rates are high right now, so is home equity. Here’s what you need to know.

Bankrate explains exactly what equity is and how it grows:

“Home equity is the portion of your home that you’ve paid off and own outright. It’s the difference between what the home is worth and how much is still owed on your mortgage. As your home’s value increases over the long term and you pay down the principal on the mortgage, your equity stake grows.”

In other words, equity is how much your home is worth now, minus what you still owe on your home loan.

How Much Equity Do Homeowners Have Now?

Recently, your equity has been growing faster than you might think. To help contextualize just how much the average homeowner has, CoreLogic says:

“. . . the average U.S. homeowner now has about $290,000 in equity.”

That’s because, over the past few years, home prices went up significantly – and those rising prices helped your equity to accumulate faster than usual. While the market has started to normalize, there are still more people wanting to buy homes than there are homes available for sale. This high demand is causing home prices to go up again.

According to the Federal Housing Finance Agency (FHFA), the Census, and ATTOM, a property data provider, nearly two-thirds (68.7%) of homeowners have either fully paid off their mortgages or have at least 50% equity (see chart below):

That means nearly 70% of homeowners have a tremendous amount of equity right now.

How Equity Helps with Your Affordability Concerns

With today’s affordability challenges, your equity can make a big difference when you decide to move. After you sell your house, you can use the equity you’ve built up in your home to help you buy your next one. Here’s how:

- Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy a new house without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates. The National Association of Realtors (NAR) states:

“These all-cash home buyers are happily avoiding the higher mortgage interest rates . . .”

- Make a larger down payment: Your equity could be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much money so today’s rates become less of a sticking point. Experian explains:

“Increasing your down payment lowers your principal loan amount and, consequently, your loan-to-value ratio, which could lead to a lower interest rate offer from your lender.”

Bottom Line

If you’re thinking about moving, the equity you’ve built up can make a big difference, especially today. To find out how much equity you’ve got in your current house and how you can use it for your next home, give me a shout!

Are More Homes Coming onto the Market?

An important factor shaping today’s market is the number of homes for sale. And, if you’re considering whether or not to list your house, that’s one of the biggest advantages you have right now. When housing inventory is this low, your house will stand out, especially if it’s priced right.

But there are some early signs that more listings are coming. According to the latest data, new listings (homeowners who just put their house up for sale) are trending up. Here’s a look at why this is noteworthy and what it may mean for you.

More Homes Are Coming onto the Market than Usual

It’s well known that the busiest time in the housing market each year is the spring buying season. That’s why there’s a predictable increase in the volume of newly listed homes throughout the first half of the year. Sellers are anticipating this and ramping up for the months when buyers are most active. But, as the school year kicks off and as the holidays approach, the market cools. It’s what’s expected.

But here’s what’s surprising. Based on the latest data from Realtor.com, there’s an increase in the number of sellers listing their houses later this year than usual. A peak this late in the year isn’t typical. You can see both the normal seasonal trend and the unusual August in the graph below:

As Realtor.com explains:

“While inventory continues to be in short supply, August witnessed an unusual uptick in newly listed homes compared to July, hopefully signaling a return in seller activity heading toward the fall season . . .”

While this is only one month of data, it’s unusual enough to note. It’s still too early to say for sure if this trend will continue, but it’s something you’ll want to stay ahead of if it does.

What This Means for You

If you’ve been putting off selling your house, now may be the sweet spot to make your move. That’s because, if this trend continues, you’ll have more competition the longer you wait. And if your neighbor puts their house up for sale too, it means you may have to share buyers’ attention with that other homeowner. If you sell now, you can beat your neighbors to the punch.

But, even with more homes coming onto the market, the market is still well below normal supply levels. That inventory deficit isn’t going to be reversed overnight. The graph below helps put this into context, so you can see the opportunity you still have now:

Bottom Line

Even though inventory is still low, you don’t want to wait for more competition to pop up in your neighborhood. You still have an incredible opportunity if you sell your house today.