Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Housing Challenge or Housing Opportunity? It Depends.

The biggest challenge in real estate today is the lack of available homes for sale. The low housing supply has caused homes throughout the country to appreciate at a much faster rate than what we’ve experienced historically.

There are many reasons for the limited number of homes on the market, but as you can see in the graph below, we’re well below where we’ve been for most of the past 10 years. Today, across the country, there is only a 2.4-month supply of homes available for sale.

The Opportunity

This lack of homes for sale is creating a challenge for many buyers who are growing frustrated in their search. On the other hand, this is a huge opportunity for sellers as low supply is driving up home values. According to CoreLogic, the average home has appreciated by more than $50,000 over the past year. And for many homeowners, that’s opening new doors as they re-think their needs and use their equity to move up or downsize.

According to Dr. Frank Nothaft, Chief Economist at CoreLogic:

“The average homeowner with a mortgage has more than $200,000 in home equity as of mid-2021.”

Today, many sellers are taking advantage of low-interest rates and the equity they have in their homes to make a move.

Bottom Line

The biggest challenge in real estate is the lack of homes for sale, but this challenge is also an opportunity for sellers. If you’re thinking about selling your house, let’s connect to start the process.

Your Home Equity Is Growing

![Your Home Equity Is Growing [INFOGRAPHIC] | MyKCM](data:image/png;base64,iVBORw0KGgoAAAANSUhEUgAABBYAAAeAAQMAAABAO0YqAAAABlBMVEUAAAD///+l2Z/dAAAAAXRSTlMAQObYZgAAAAlwSFlzAAAOxAAADsQBlSsOGwAAAQxJREFUeNrtwTEBAAAAwqD1T20JT6AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAOBv3i0AAcU8YjoAAAAASUVORK5CYII=)

Some Highlights

![Your Home Equity Is Growing [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/10/18091034/20211022-MEM-1046x2053.png)

- If you’re a homeowner, today’s rising equity is great news. On average, homeowners have gained $51,500 in equity since this time last year.

- Whether it’s funding an education, fueling your next move, or starting a business, your home equity is a great tool you can use to power your dreams.

- Ready to sell? Let’s connect to talk about how you can take advantage of your rising equity to reach your goals.

What Does the Future Hold for Home Prices?

If you’re looking to buy or sell a house, chances are you’ve heard talk about today’s rising home prices. And while this increase in home values is great news for sellers, you may be wondering what the future holds. Will prices continue to rise with time, or should you expect them to fall?

To answer that question, let’s first understand a few terms you may be hearing right now.

- Appreciation is an increase in the value of an asset.

- Depreciation is a decrease in the value of an asset.

- Deceleration is when something happens at a slower pace.

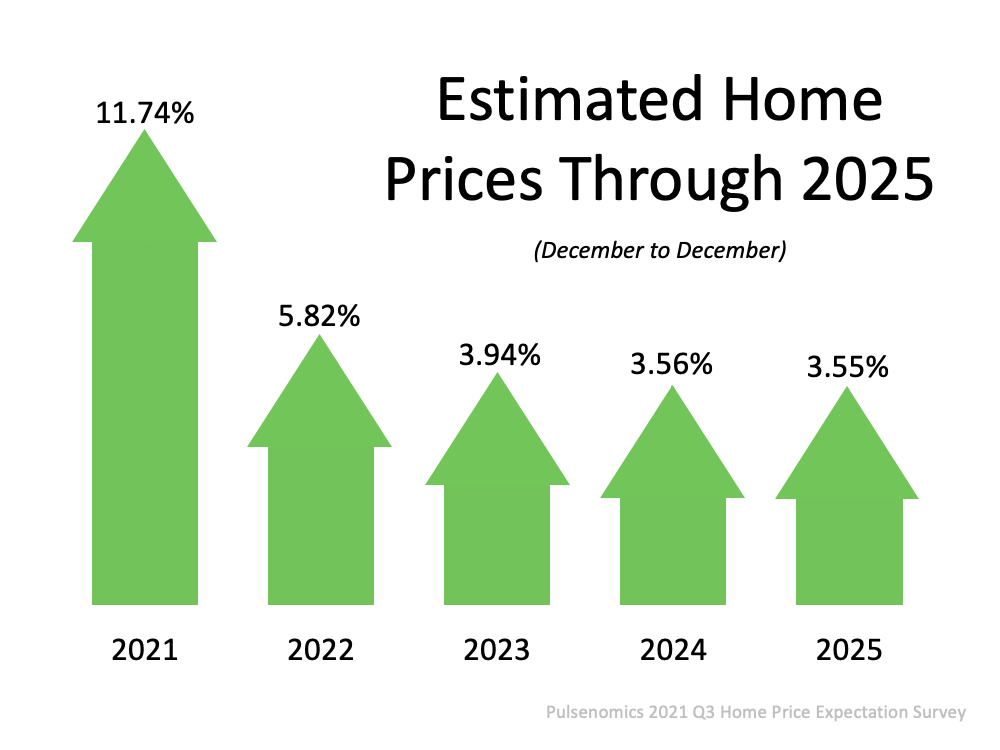

It’s important to note home prices have increased, or appreciated, for 114 straight months. To find out if that trend may continue, look to the experts. Pulsenomics surveyed over 100 economists, investment strategists, and housing market analysts asking for their five-year projections. In terms of what lies ahead, experts say the market may see some slight deceleration, but not depreciation.

Here’s the forecast for the next few years: As the graph above shows, prices are expected to continue to rise, just not at the same pace we’ve seen over the last year. Over 100 experts agree, there is no expectation for price depreciation. As the arrows indicate, each number is an increase, which means prices will rise each year.

As the graph above shows, prices are expected to continue to rise, just not at the same pace we’ve seen over the last year. Over 100 experts agree, there is no expectation for price depreciation. As the arrows indicate, each number is an increase, which means prices will rise each year.

Bill McBride, author of the blog Calculated Risk, also expects deceleration, but not depreciation:

“My sense is the Case-Shiller National annual growth rate of 19.7% is probably close to a peak, and that year-over-year price increases will slow later this year.”

Ivy Zelman of Zelman & Associates agrees, saying:

“. . . home price appreciation is on the cusp of flipping to a decelerating trend.”

A recent article from realtor.com indicates you should expect:

“. . . annual price increases will slow to a more normal level, . . .”

What Does This Deceleration Mean for You?

What experts are projecting for the years ahead is more in line with the historical norm for appreciation. According to data from Black Knight, the average annual appreciation from 1995-2020 is 4.1%. As you can see from the chart above, the expert forecasts are closer to that pace, which means you should see appreciation at a level that’s aligned with a more normal year.

If you’re a buyer, don’t expect a sudden or drastic drop in home prices – experts say it won’t happen. Instead, think about your homeownership goals and consider purchasing a home before prices rise further.

If you’re a seller, the continued home price appreciation is good news for the value of your house. Work with an agent to list your house for the right price based on market conditions.

Bottom Line

Experts expect price deceleration, not price depreciation over the coming years.

Homebuyer Tips for Finding the One

Some Highlights

Some Highlights

- The best advice carries across multiple areas of life. When it comes to homebuying, a few simple tips can help you stay on track.

- Because of increased demand, you’ll need to be patient and embrace compromises during your search. Then, once you’ve fallen in love, commit by putting your best offer forward.

- If you’re looking to buy a home this year, let’s connect so you have a dedicated partner and teammate to help you find the one.

Don’t Wait for a Lower Mortgage Rate – It Could Cost You

Today’s housing market is truly one for the record books. Over the past year, we’ve seen the lowest mortgage rates in history. And while those rates seemed to bottom out in January of this year, the golden window of opportunity for buyers isn’t over just yet. If you’re one of the buyers who worry they’ve missed out, rest assured today’s mortgage rates are still worth taking advantage of.

Even today, our mortgage rates are below what they’ve been in recent decades. So, while you may not be able to lock in the rate your friend got recently, you’re still in a great position to secure a rate well below what your parents and even grandparents got in years past. The key will be acting sooner rather than later.

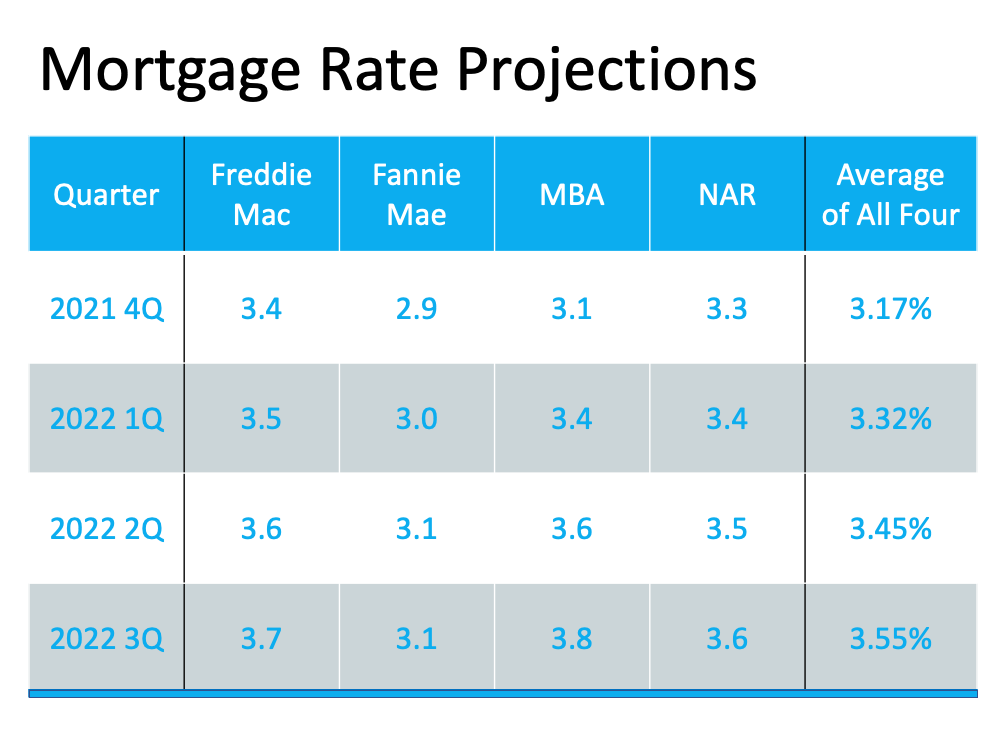

In late September, mortgage rates ticked above 3% for the first time in months. And according to experts throughout the industry, mortgage rates are projected to continue rising in the months ahead. Here’s where experts say rates are headed: While a projected half percentage point increase may not seem substantial, it does have an impact when you’re buying a home. When rates rise even slightly, it affects how much you’ll pay month-to-month on your home loan. The chart below shows how it works:

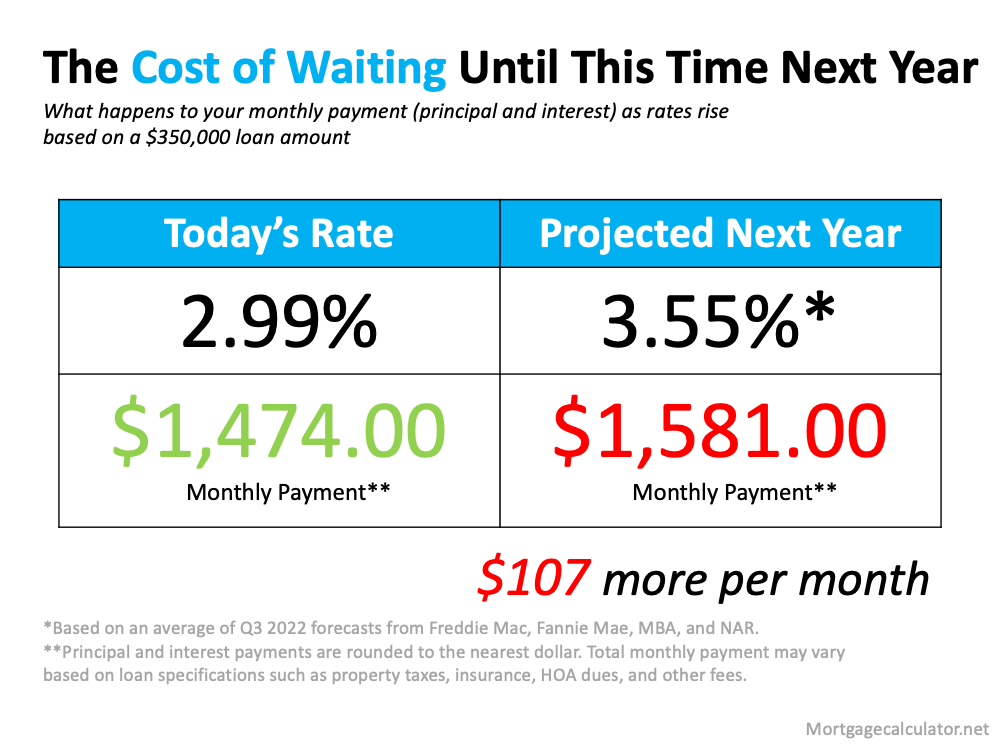

While a projected half percentage point increase may not seem substantial, it does have an impact when you’re buying a home. When rates rise even slightly, it affects how much you’ll pay month-to-month on your home loan. The chart below shows how it works: In this example, if rates rise to 3.55%, you’ll pay an extra $100 each month on your monthly mortgage payment if you purchase a home around this time next year. That extra money can really add up over the life of a 15 or 30-year loan.

In this example, if rates rise to 3.55%, you’ll pay an extra $100 each month on your monthly mortgage payment if you purchase a home around this time next year. That extra money can really add up over the life of a 15 or 30-year loan.

Clearly, today’s mortgage rates are worth taking advantage of before they climb further. The rates we’re seeing right now give you a unique opportunity to afford more home for your money while keeping your monthly payment down.

Bottom Line

Waiting for a lower mortgage rate could cost you. Experts project rates will continue to rise in the months ahead.

What Do Supply and Demand Tell Us About Today’s Housing Market?

There’s a well-known economic theory – the law of supply and demand – that explains what’s happening with prices in the current real estate market. Put simply, when demand for an item is high, prices rise. When the supply of the item increases, prices fall. Of course, when demand is very high and supply is very low, prices can rise significantly.

Understanding the impact both supply and demand have can provide the answers to a few popular questions about today’s housing market:

- Why are prices rising?

- Where are prices headed?

- What does this mean for homebuyers?

Why Are Prices Rising?

According to the latest Home Price Insights report from CoreLogic, home prices have risen 18.1% since this time last year. But what’s driving the increase?

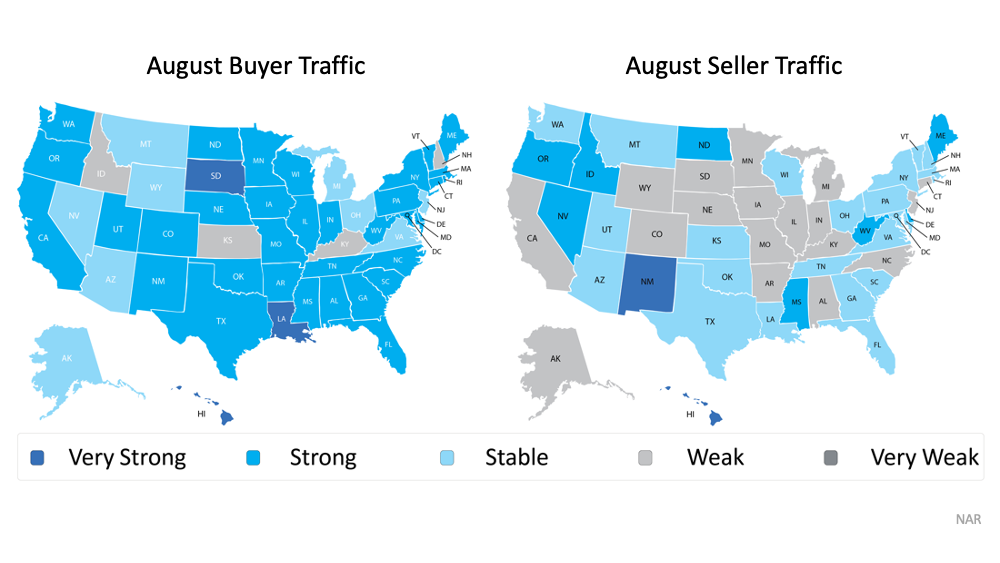

Recent buyer and seller activity data from the National Association of Realtors (NAR) helps answer that question. When we take NAR’s buyer activity data and compare it to the seller traffic during the same timeframe, we can see buyer demand continues to outpace seller activity by a wide margin. In other words, the demand for homes is significantly greater than the current supply that’s available to buy (see maps below): This combination of low supply and high demand is what’s driving home prices up. Bill McBride, author of the Calculated Risk blog, puts it best, saying:

This combination of low supply and high demand is what’s driving home prices up. Bill McBride, author of the Calculated Risk blog, puts it best, saying:

“By some measures, house prices seem high, but the recent price increases make sense from a supply and demand perspective.”

Where Are Prices Headed?

The supply of homes for sale will greatly affect where prices head over the coming months. Many experts forecast prices will continue to increase, but they’ll likely appreciate at a slower rate.

Buyers hoping to purchase the home of their dreams may see this as welcome news. In this case, perspective is important: a slight moderation of home prices does not mean prices will depreciate or fall. Price increases may occur at a slower pace, but experts still expect them to rise.

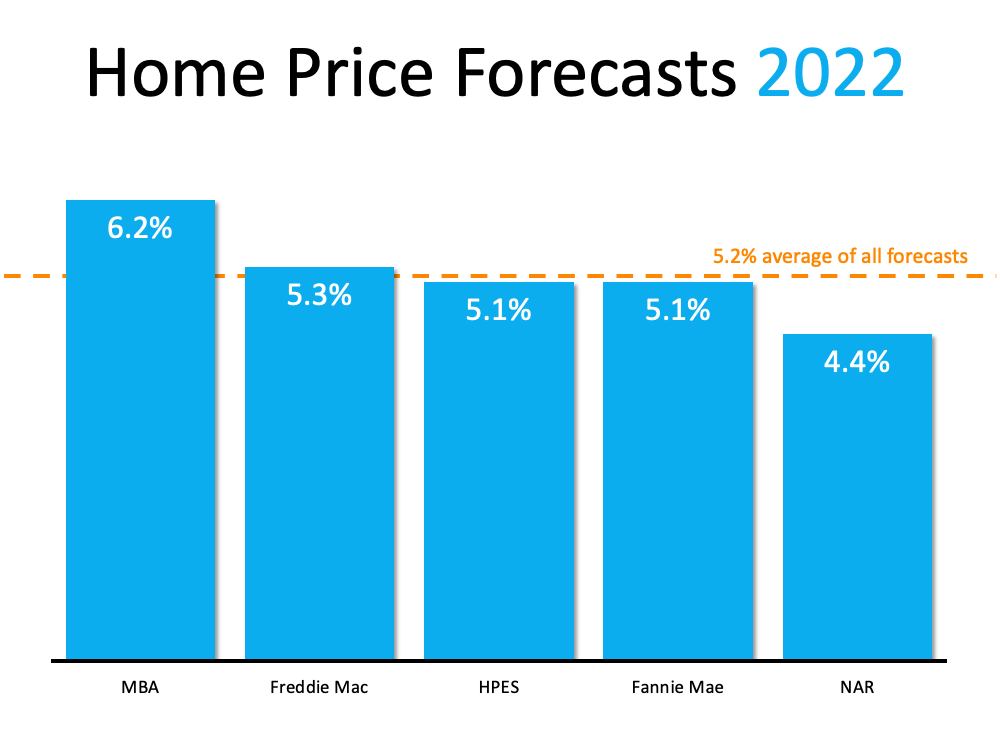

Five major entities that closely follow the real estate market forecast home prices will continue appreciating through 2022 (see graph below):

What Does This Mean for Homebuyers?

If you’re waiting to enter the market because you’re expecting prices to drop, you may end up paying more in the long run. Even if price increases occur at a slower rate next year, prices are still projected to rise. That means the home of your dreams will likely cost even more in 2022.

Bottom Line

The truth is, high demand and low supply are what’s driving up home prices in today’s housing market. And while prices may increase at a slower pace in the coming months, experts still expect them to rise.

The Main Key To Understanding the Rise in Mortgage Rates

Every Thursday, Freddie Mac releases the results of their Primary Mortgage Market Survey which reveals the most recent movement in the 30-year fixed mortgage rate. Last week, the rate was announced as 3.01%. It was the first time in three months that the mortgage rate surpassed 3%. In a press release accompanying the survey, Sam Khater, Chief Economist at Freddie Mac, explains:

“Mortgage rates rose across all loan types this week as the 10-year U.S. Treasury yield reached its highest point since June.”

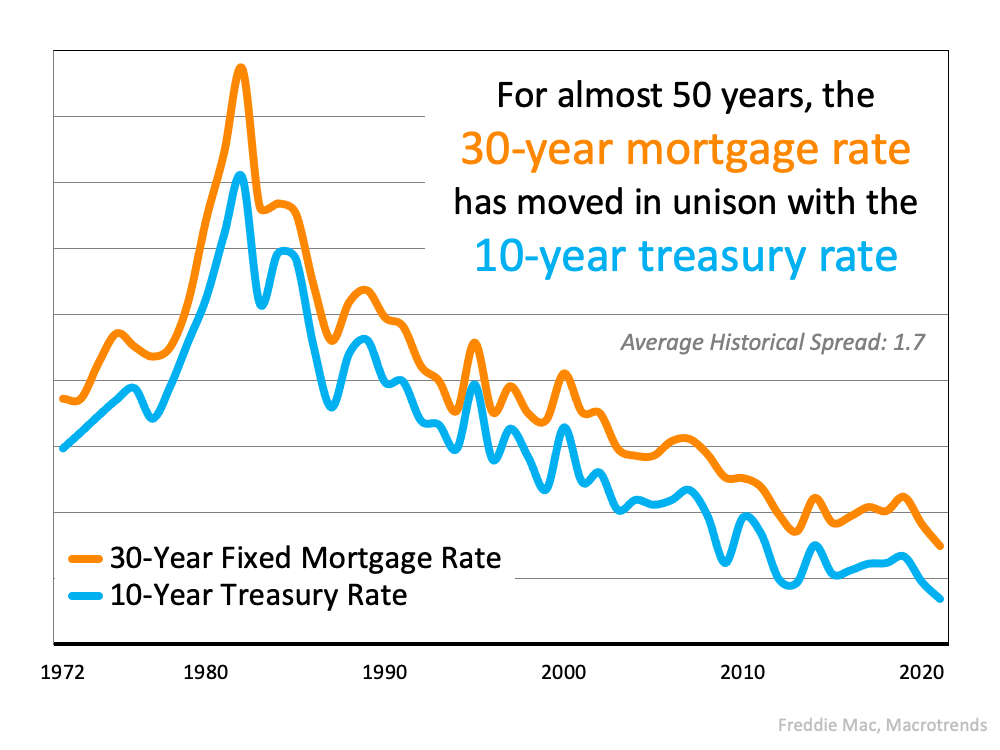

The reason Khater mentions the 10-year U.S. Treasury yield is because there has been a very strong relationship between the yield and the 30-year mortgage rate over the last five decades. Here’s a graph showing that relationship: The relationship has also been consistent throughout 2021 as evidenced by this graph:

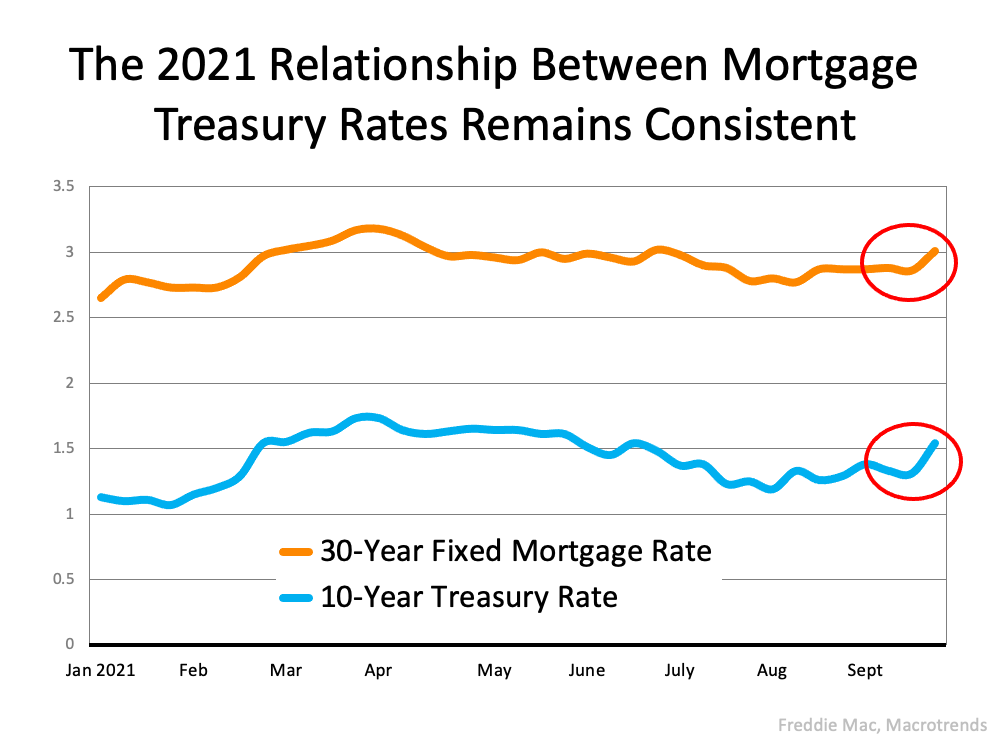

The relationship has also been consistent throughout 2021 as evidenced by this graph: The graph also reveals the most recent jump in mortgage rates was preceded by a jump in the 10-year Treasury rate (called out by the red circles).

The graph also reveals the most recent jump in mortgage rates was preceded by a jump in the 10-year Treasury rate (called out by the red circles).

So, What Impacts the Yield Rate?

According to Investopedia:

“There are a number of economic factors that impact Treasury yields, such as interest rates, inflation, and economic growth.”

Since there are currently concerns about inflation and economic growth due to the pandemic, the Treasury yield spiked last week. That spike impacted mortgage rates.

What Does This Mean for You?

Khater, in the Freddie Mac release mentioned above, says:

“We expect mortgage rates to continue to rise modestly which will likely have an impact on home prices, causing them to moderate slightly after increasing over the last year.”

Nadia Evangelou, Senior Economist and Director of Forecasting for the National Association of Realtors (NAR), also addresses the issue:

“Consumers shouldn’t panic. Keep in mind that even though rates will increase in the following months, these rates will still be historically low. The National Association of REALTORS forecasts the 30-year fixed mortgage rate to reach 3.5% by mid-2022.”

Bottom Line

Forecasting mortgage rates is very difficult. As Mark Fleming, Chief Economist at First American once quipped:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

That being said, if you’re either a first-time homebuyer or a current homeowner thinking of moving into a home that better fits your current needs, keep abreast of what’s happening with mortgage rates. It may very well impact your decision.